Key takeaways

HMRC brings in new compliance obligations for umbrella companies

End-users must understand when liability for PAYE and NIC applies.

Clear contractual arrangements will be critical

Businesses should review agreements to avoid unexpected tax exposure.

New operational and financial risk to manage

Training and audits can ensure compliance with changes.

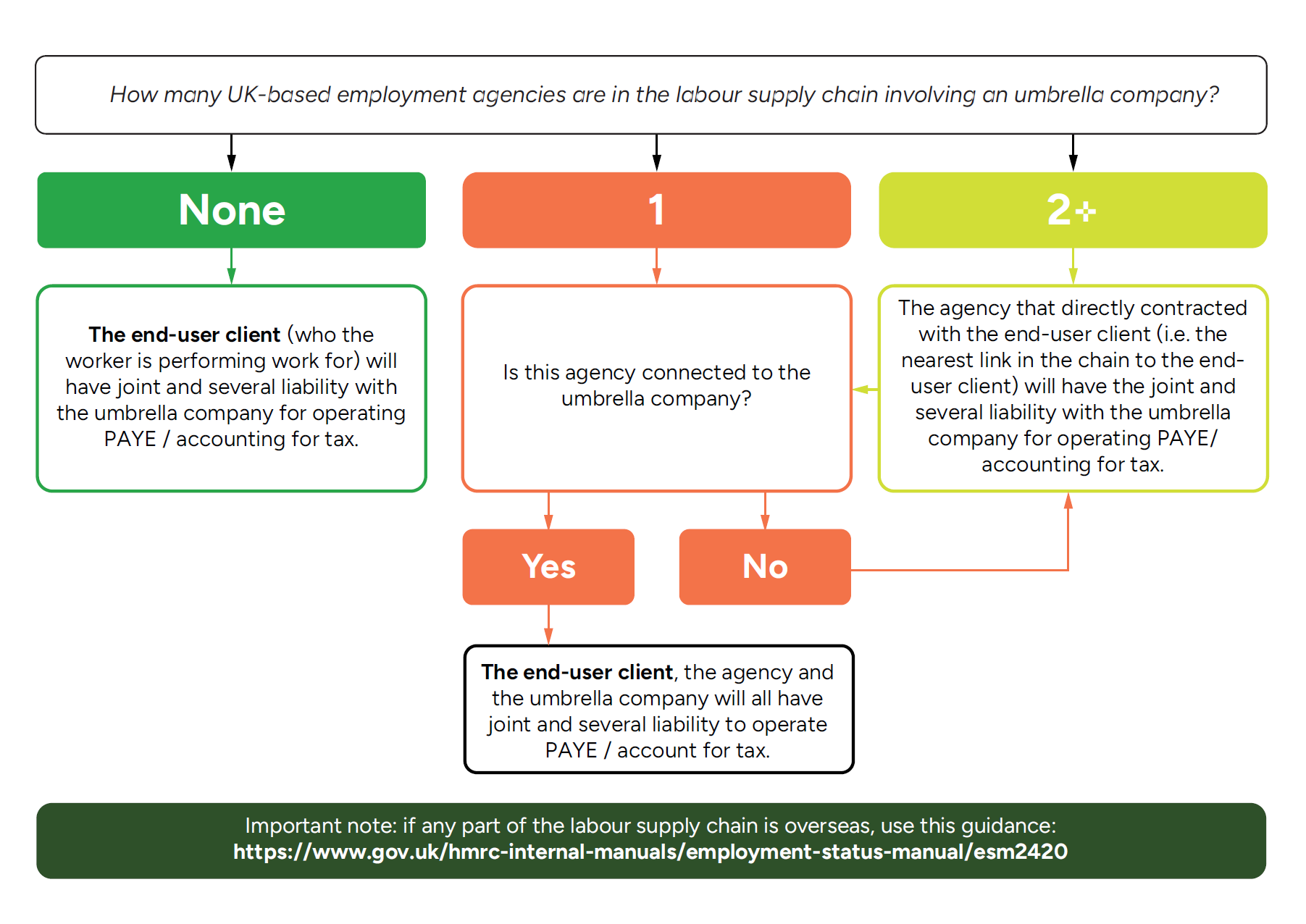

As we have highlighted previously, the government has committed to regulate the legal status and tax position of umbrella companies from 6 April 2026. Umbrella companies legally ‘employ’ individuals and then supply them to work for end clients. Previously, the umbrella company had the sole legal responsibility to operate PAYE.

In relation to any money paid to workers employed by an umbrella company on or after 6 April 2026, under the new rules, although the umbrella company still has the primary duty to operate PAYE, joint responsibility for operating PAYE now rests with either the employment agency (where applicable) or the end-user client (depending on the circumstances).

To help employers in a labour supply chain which includes an umbrella company to adapt to the changes, HMRC has recently published guidance on the new PAYE rules for labour supply chains that include umbrella companies.

This guidance highlights that the new rules apply:

to new and existing labour supply chains; and

in relation to any money paid on or after 6 April 2026 to workers employed by an umbrella company.

In labour supply chains which do not involve an overseas intermediary, in summary the rules now apply as follows:

Where an umbrella company has not paid the correct amount of PAYE to HMRC, any unmet tax liability will be recovered from whichever entity in the supply chain is jointly and severally liable under the new rules.

Separate guidance applies if any part of the labour supply chain is non-UK based.